On this page, you can learn more about the company's commitment. You will find information about the history of the commitment, its scope, and the climate protection projects it supports.

| Key Facts | |

|---|---|

| Cooperation since: | 2025 |

| CO₂ emissions in tons since the start of the partnership: | 50 |

| Savings compared to the previous year (2026 vs. 2025): | t.b.a. |

| Scope of contribution: | Scopes 1, 2 & 3 |

| Relevant Scope 3 emissions not included in the scope of the contribution: | 3.1, 3.3, 3.6, 3.7 |

| Label number: | PK-DE-00781 |

ITB Consulting GmbH advises a large number of companies and their employees from a wide range of industries. The large team strives to provide expert, solution-oriented support and advice for customer projects. ITB Consulting GmbH attaches great importance to practicing climate protection within the company. To this end, it offers its employees financial support for the “Deutschlandticket” to encourage the use of public transportation. Local and long-distance public transport is also used as a priority for business travel. For journeys that have to be made by car, the company uses a car-sharing fleet that is certified with the “Blue Angel” eco-label. ITB also purchases green electricity. Since 2025, the company has been accounting for all emissions that arise directly at its site or indirectly through energy consumption at the site. For this, the company has been awarded the PRIMAKLIMA label “Climate Protection Contribution Scope 1, 2 & 3.”

What we have already achieved together:

| Year | Scope of contribution | Link CCF | Accounting method | CO₂ tons included | +/- compared to previous year | Project |

|---|---|---|---|---|---|---|

| 2026 | Scope 1, 2 & 3 | GHG Protocol | 50 (prognosis) | t.b.a. | Papua New Guinea | |

| 2025 | Scope 1, 2 & 3 | Link 1 | GHG Protocol | 50 (prognosis) | t.b.a. | Papua New Guinea |

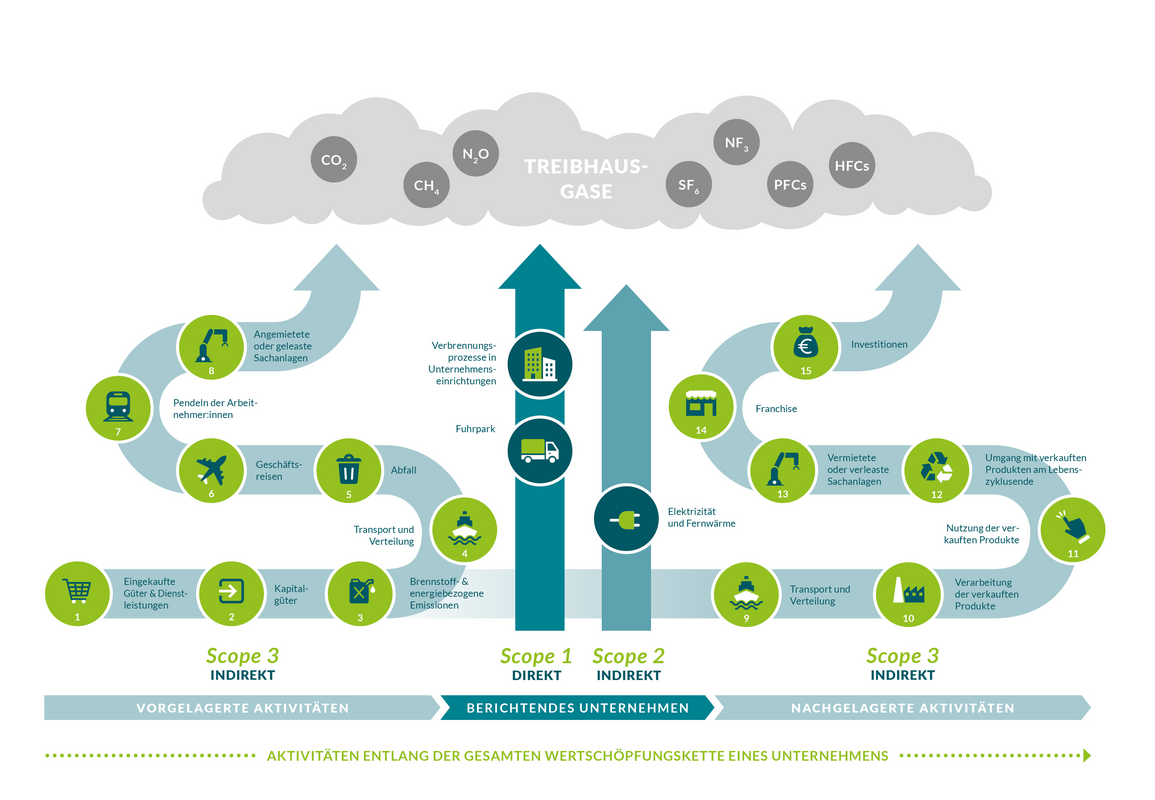

Understanding and specifically reducing your carbon footprint Scope 1, 2 and 3:

When it comes to carbon footprints, Scope 1 and 2 play the leading roles: these are the emissions that arise directly and indirectly at the company's location.

However, only by comprehensively considering Scope 1, 2, and 3 can a company's total climate impact be revealed. This transparency forms the basis for targeted emission reductions and the development of a sustainable, future-proof strategy.

Scope 1 – Directly reducing emissions

Scope 1 covers all emissions generated directly at the site as a result of the company's own activities at the company location – such as the combustion of fuels in company-owned vehicles, heating systems, and machines, or coolant losses from air conditioning systems. This is where companies can take immediate action: switching to low-emission technologies, more efficient heating systems, or alternative drive systems will result in direct improvements.

Scope 2 – Making energy consumption climate-friendly

Scope 2 covers indirect emissions generated during the production of purchased energy such as electricity or (district) heating. Since the emissions are not generated on site but are part of activities at the company's own location, they are not included in Scope 3. Switching to certified renewable energies reduces emissions to zero.

Scope 3 – Include the value chain

Scope 3 considers all upstream and downstream indirect emissions along the value chain – from raw material procurement, transport, use, and disposal of products to business travel and investments. Through sustainable supply chains, efficient processes, and climate-friendly materials, companies can make a far-reaching contribution to climate protection together with their partners.

Further information

Deutschsprachige Infos zu ITB Consulting GmbH

Hier erfahren Sie mehr über das Engagement des Unternehmens. Sie finden Informationen über die Historie des Engagements, den Umfang und die unterstützten Klimaschutzprojekte.

| Key Facts | |

|---|---|

| Kooperation seit: | 2025 |

| CO₂-Emissionen in Tonnen: seit Kooperationsbeginn: | 50 |

| Einsparung zum Vorjahr (2025 ggü. 2024): | t.b.a. |

| Beitragsumfang: | Scopes 1, 2 & 3 |

| Relevante Scope 3-Emissionen, die nicht im Beitragsumfang enthalten sind: | 3.1, 3.3, 3.6, 3.7 |

| Labelnummer: | PK-DE-00781 |

Die ITB Consulting GmbH berät eine Vielzahl von Unternehmen und deren Mitarbeitenden aus den unterschiedlichsten Branchen. Das große Team bemüht sich um eine fachlich kompetente und lösungsorientierte Begleitung und Beratung der Kund:innenprojekte. Der ITB Consulting GmbH ist es wichtig, den Klimaschutz im Unternehmen zu leben. Dafür bietet sie ihren Mitarbeitenden eine finanzielle Unterstützung für das Deutschlandticket an. Der öffentliche Nah- und Fernverkehr wird vorrangig auch bei Geschäftsreisen genutzt. Für Strecken, die mit dem Auto zurückgelegt werden müssen, nutzt das Unternehmen eine Carsharing-Flotte, die mit dem Umweltzeichen „Blauer Engel“ zertifiziert ist. Des Weiteren bezieht ITB Ökostrom. Somit bilanziert das Unternehmen seit dem Jahr 2025 alle Emissionen, die direkt am Standort entstehen oder indirekt durch den Energieverbrauch am Standort verursacht werden. Dafür erhält das Unternehmen das PRIMAKLIMA-Label „Klimaschutzbeitrag Scope 1, 2 & 3“.

Was wir gemeinsam schon bewirken konnten:

| Jahr | Beitragsumfang | Link CCF | Methode der Bilanzierung | Eingebundene Tonnen CO₂ | +/- zum Vorjahr | Projekt |

|---|---|---|---|---|---|---|

| 2026 | Scope 1, 2 & 3 | GHG Protocol | 50 (Prognose) | t.b.a. | Papua-Neuguinea | |

| 2025 | Scope 1, 2 & 3 | Link 1 | GHG Protocol | 50 (Prognose) | t.b.a. | Papua-Neuguinea |

Den CO₂-Fußabdruck verstehen und gezielt reduzieren Scope 1, 2 und 3:

Wenn’s um den CO₂-Fußabdruck geht, spielen Scope 1 und 2 die Hauptrollen: Das sind die Emissionen, die direkt und indirekt am Unternehmensstandort entstehen.

Doch erst mit der umfassenden Betrachtung von Scope 1, 2 und 3 wird die gesamte Klimawirkung eines Unternehmens sichtbar. Diese Transparenz bildet die Grundlage, um gezielt Emissionen zu reduzieren und eine nachhaltige, zukunftsfähige Strategie zu entwickeln.

Scope 1 – Direkte Emissionen unmittelbar reduzieren

Scope 1 umfasst alle direkt am Standort entstehenden Emissionen, die durch eigene Aktivitäten am Unternehmensstandort entstehen – etwa die Verbrennung von Kraftstoffen in firmeneigenen Fahrzeugen, Heizungen und Maschinen oder auch durch Kühlmittelverluste aus Klimaanlagen. Hier können Unternehmen unmittelbar ansetzen: Der Umstieg auf emissionsarme Technologien, effizientere Heizsysteme oder alternative Antriebe sorgt für direkte Verbesserungen.

Scope 2 – Energieverbrauch klimagerecht gestalten

Scope 2 erfasst die indirekten Emissionen, die bei der Erzeugung von eingekaufter Energie wie Strom oder (Fern-)Wärme entstehen. Da die Emissionen nicht vor Ort entstehen, aber zu Aktivitäten am eigenen Standort zählen, werden sie nicht zu Scope 3 gerechnet. Der Wechsel zu zertifiziert erneuerbaren Energien setzt die Emissionen auf null.

Scope 3 – Wertschöpfungskette einbeziehen

Scope 3 betrachtet alle vor- und nachgelagerten, indirekten Emissionen entlang der Wertschöpfungskette – von der Rohstoffbeschaffung über Transport, Nutzung und Entsorgung der Produkte bis hin zu Geschäftsreisen und Investitionen. Durch nachhaltige Lieferketten, effiziente Prozesse und klimafreundliche Materialien können Unternehmen gemeinsam mit ihren Partnern einen weitreichenden Beitrag zum Klimaschutz leisten.